A few caveats are necessary for the paper, first being to note that it’s a draft that hasn’t yet been subject to peer review.

Second, University of Chicago Assistant Professor of Accounting John Barrios and his partners say that “Uber and Lyft declined to provide data on driver enrollment and usage for this project” and that instead they measured the degree of app adoption by extrapolating from Google searches “for rideshare keywords,” which other research has highlighted as a useful indicator for increased use. In response to the paper, an Uber spokesperson emphasized the preliminary and non-peer reviewed nature of the findings and deferred to City Observatory Director Joe Cortright’s response expressing skepticism about the findings, citing three alleged shortfalls in the methodology:

– The study leaves out the effect of lower gas prices and increased driving on crash rates.

– Rural areas–which essentially don’t have ride-hailing services–saw even bigger increases in crashes than cities with ride-hailing.

– And the study doesn’t try to correlate the increase in crashes to either the times or the places that ride-hailed vehicles are most used, which would be a much more powerful indicator of a safety effect.

Cortright does not dismiss the Chicago research but does contend that more analysis is needed before accepting its conclusions. Barrios also protests that the reference to rural accidents is “misleading” because it refers to national averages rather than area-specific analysis.

“You can’t use national averages to talk about causal effects,” said Barrios via email, indicating that the next draft of the study will include material relevant to these critiques.

// Illustration by Amelia Giller

Could This Be The End of the Taxi Era? You Can Thank SFMTA For That // Published 11/09/18

It’s the tell-of-age story we all hear again and again, businesses fall as technology continues to soar. For the taxi industry, they may have more on their plate than first expected.

When Lyft and Uber were first invented, used, and accepted by the popular mainstream of San Francisco, the taxi service began to suffer with little stabs to the abdomen. When 2016 rolled around, Yellow Cab filed for chapter 11 bankruptcy protection, stating the ride-sharing applications began to bleed their companies dry on top of all the allegations the company alone faced.

BUT. SF Federal Credit Union accuses SFMTA of allowing Uber, Lyft to kill cabs and taxi-permit sale program—but not before making $64 million this past fiscal year. Why is this you may ask? Permitting. How does permitting affect SF taxi and cab drivers, well we will explain, putting a taxicab out for hire on the streets requires a city-issued permit, called a “medallion.” A medallion essentially was the golden ticket of monetary value for drivers in the city. Again, pre-Lyft and Uber. The city could award these medallions to drivers at a low price, and when the driver held onto these permitted medallions, they could resale them for a higher cost. But to sell these assets at a fixed price of $250,000 to cab drivers paid mostly in cash, the SFMTA needed a lending partner.

Now enters in the SF Federal Credit Union, in a newly-founded ride-sharing city, they would be the only ones to finance the medallion system in 2017. The credit union would finance loans needed for medallion sales. Drivers would pay about $1,200 a month—in most cases, no more than 20 percent of their earnings. But with making nearly $64 million in 2016, SFMTA was to do what it could to ensure that a permit to drive a taxi in San Francisco remained a valuable asset.

Today, city streets are now home to thousands of privately-owned personal vehicles driving for Uber and Lyft. Taxicab medallions are now worthless. The city hasn’t sold a medallion in nearly two years. Which means SFMTA is severely screwed and SF Federal Credit Union has bled money into another’s wound. So bad so that drivers who own a city medallion now are owners of toxic currency: drivers unlucky enough to have bought a $250,000 medallion—a loan that taxi-driver earnings guaranteed to make whole within ten years—now can’t cover their monthly loan payments.

In a lawsuit filed by the San Francisco Federal Credit Union in San Francisco Superior Court: the fault of this rests in SFMTA’s court which allegedly failed to regulate, thereby allowing Uber and Lyft to take over. The suit seeks $28 million in damages from the city, money it will attempt to convince a jury to award. “They stuck their head in the sand,” said Oliver, the credit union CEO, describing the SFMTA’s approach to Uber and Lyft destroying the taxi industry. The SFMTA’s website declares, somewhat pitifully, San Francisco as a “taxi town”—and describes its mission as promoting a “vibrant” taxi industry. HA. Hilarious.

As assets began to crumble in 2013, after various complaints from credit union officials and taxi drivers alike, SFMTA stood by and let everything fall to the ground without issuing refunds and regulations to the now worthless medallions. The SFMTA also brushed off concerns from the credit union—promising at one time to alter the sales program to ameliorate the credit union’s concerns after it conducted a study. No study was ever launched.

So where are we now? Wednesday, the lawsuit was filed in San Francisco superior court and if the credit union’s lawsuit is successful, the SFMTA could be made to buy all of the taxicab medallions sold with credit union financing, a hit of millions of dollars. Yep.

With Yellow Cab filing for chapter 11 Bankruptcy Protection, one must question if we’re seeing the end of those iconic yellow speed wagons.

Coming at no shock or attention rather, San Francisco’s biggest taxi operator Yellow Cab has just filed for chapter 11 bankruptcy protection. What does that all mean however? The Yellow Cab Cooperative cited difficulties including competition from app-based ride-sharing services, namely Uber and Lyft. Coming at no surprise because in 2016, who gets in a cab willingly anymore?

The cab cooperation states that with the amount of accident-related costs and the decline in ridership, it’s not making ends meet like they used too. “In June, a jury awarded $8.1 million to a woman who was partially paralyzed in a Yellow Cab accident, court paper show, and the company said it faces some 150 open claims valued as high as $10 million.” – WSJ. But do you think that having these little yellow metal boxes driving all around the city is still a good move for the company, or for us?

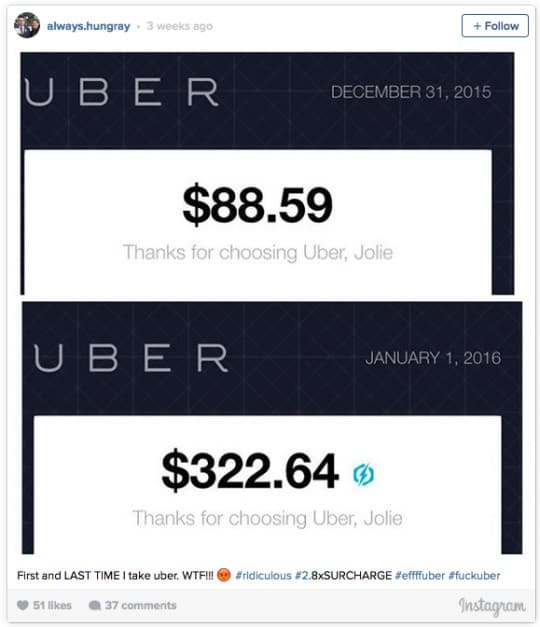

We recently read an article online about the disaster of NYE Uber rides. People woke up from their blissful alcohol induced naps to a stunning charge on their mobile banking apps, what should have been a $20 dollar ride ended up being a $200 ride at the end of the evening. People were definitely turning back into their pumpkins.

commenter stated that, “Shoutout to everyone who saw the 6x uber surge pricing last night and still forgot regular taxis exist.”

But that’s the beauty of being on the move right? No more standing in the rain as multiple dim taxi lights speed past you. No more ridiculous tip prices and being verbally assaulted for not paying their suggested rate. Call a car at the press of a button and it’ll whisk you away to your destination.

As we move into the technological, we slip away from the traditional. One commenter on WSJ had this to say, “Adapt or die.” With the constant need for upgrading and providing even quicker services, companies such as Yellow Cab, have fallen back to big banks for funding protection. CitiBank commented, “’nontraditional ride-sharing companies’ would have on the city’s traditional medallion-based business model.Lending money to taxicab companies that possess medallions has historically been a safe business, but the market has tightened as major lenders worry how the new competitors will affect the business.“

Sadly, in our defense, we only take taxi’s when our app’s aren’t responding. C’est La Vie, Yellow Cab, we will attend the funeral in time.

What are your thoughts? Are you still taking cabs because you’re “city chic?” Tell us on our FB Page.

// Images sourced from CR Fashion Book and Buzzfeed, sources sourced from The Wall Street Journal and Buzzfeed.